How to Claim Hotel Expenses Through Your Travel Insurance Provider

Understanding Your Travel Insurance Policy

Before attempting to claim hotel expenses, thoroughly understanding your travel insurance policy is crucial. Policies vary significantly in their coverage, terms, and conditions. Familiarizing yourself with the specific details of your plan will prevent disappointment and streamline the claims process. This includes understanding what constitutes a covered event and what documentation is required to support your claim.

Hotel Expense Reimbursement Clauses

Travel insurance policies typically include clauses specifying the circumstances under which hotel expenses will be reimbursed. These clauses often stipulate that the expenses must be directly related to a covered event, such as a trip delay or a natural disaster forcing you to extend your stay. The policy may also set limits on the amount of reimbursement per day or for the total duration of the unforeseen hotel stay. Furthermore, it is essential to check if pre-authorization is required before incurring additional hotel expenses. Failing to do so could jeopardize your claim. Many policies explicitly exclude expenses resulting from events that are considered foreseeable or preventable, such as booking a flight at the last minute or failing to check weather forecasts before departure.

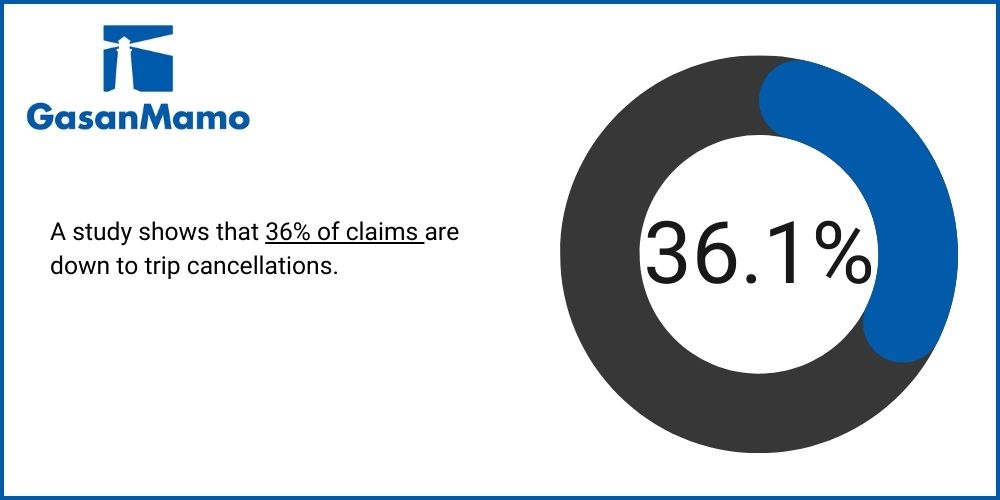

Trip Cancellation vs. Unexpected Hotel Expenses

Coverage for trip cancellations and coverage for unexpected hotel expenses during a trip are distinct. Trip cancellation coverage reimburses you for prepaid, non-refundable expenses if your trip is canceled due to a covered reason, such as a sudden illness or a natural disaster rendering your destination unsafe. This might include hotel bookings, but the focus is primarily on the overall trip cost. In contrast, coverage for unexpected hotel expenses focuses specifically on additional hotel costs incurred *during* a trip due to unforeseen circumstances, such as flight delays or medical emergencies requiring an extended stay. These are separate benefits and may have different claim procedures and limitations.

Examples of Covered and Uncovered Hotel Expenses

Several scenarios illustrate the difference between covered and uncovered hotel expenses. For instance, if a severe storm causes widespread flight cancellations, forcing you to stay an extra night at your hotel, this additional expense might be covered, provided the storm is considered a covered event under your policy. Similarly, if a medical emergency requires an extended hospital stay, leading to additional hotel nights for a family member, these costs may also be covered, subject to the policy’s limitations and the submission of relevant medical documentation. Conversely, expenses incurred due to personal negligence, such as missing a flight because of oversleeping, or expenses incurred due to events specifically excluded by the policy, such as political unrest in a known high-risk area, would generally not be covered. Always refer to the specific terms and conditions Artikeld in your policy for clarity.

Documenting Hotel Expenses

Proper documentation is crucial for a successful claim with your travel insurance provider. Failing to provide sufficient evidence can lead to delays or even rejection of your claim. This section details the necessary steps to ensure your hotel expense claim is processed smoothly. Careful record-keeping from the outset of your trip is key.

How to Claim Hotel Expenses Through Your Travel Insurance Provider – To ensure a smooth claims process, it’s vital to meticulously document all hotel-related expenses. This involves gathering and retaining all relevant paperwork. The more comprehensive your documentation, the higher the likelihood of a successful claim. Remember that insurance companies require verifiable proof of expenses.

Necessary Documentation for Claiming Hotel Expenses

A comprehensive checklist of necessary documents significantly increases your chances of a successful claim. Having all these items readily available simplifies the claims process and minimizes potential delays.

- Original hotel invoice or receipt: This is the most important piece of documentation. It should clearly show the hotel name, your name, the dates of your stay, the total cost, and any additional charges (e.g., room service, mini-bar).

- Confirmation of your hotel booking: This could be an email confirmation, a printed booking confirmation, or a screenshot of your booking from a travel website. This helps verify your stay.

- Your travel insurance policy details: This includes your policy number and the contact information for your insurance provider.

- A copy of your passport or driver’s license: This is for identification purposes and links your claim to your identity.

- Photos of the hotel and your room (optional, but helpful): These can be useful if there were any issues with the hotel or room that led to additional expenses.

Importance of Retaining Original Receipts and Invoices

Original receipts and invoices serve as irrefutable proof of your expenses. These documents provide verifiable evidence that you incurred the costs you are claiming. Copies or reconstructed statements are less likely to be accepted by insurance providers. Always keep your receipts in a safe and organized manner throughout your trip.

Original receipts are the most reliable form of evidence and are highly recommended.

Alternative Methods of Proving Expenses if Original Receipts are Lost or Unavailable

While original receipts are ideal, circumstances may arise where they are lost or unavailable. In such situations, alternative methods of proof can be considered, though they may require additional supporting documentation. It is important to be prepared for such eventualities and to take steps to mitigate the risks of losing receipts.

- Bank or credit card statements: These statements can show payments made to the hotel. However, you’ll need to provide additional supporting evidence to clearly link the payment to your hotel stay, such as a booking confirmation.

- Hotel confirmation email or online booking details: This can provide some evidence of your stay, but it might not show the exact costs incurred, particularly if there were any additional charges.

- Witness statements: While less reliable, a statement from a travel companion who can attest to your stay and expenses might be considered in exceptional circumstances. This is typically not sufficient on its own.

The Claim Process

Submitting a claim for hotel expenses covered under your travel insurance policy involves a straightforward process. However, understanding the steps and requirements will ensure a smooth and timely reimbursement. This section provides a step-by-step guide, addresses common reasons for claim rejection, and Artikels available submission methods.

Step-by-Step Claim Submission

The claim process typically involves several key steps. Careful adherence to these steps significantly increases the likelihood of a successful claim.

- Review Your Policy: Before initiating a claim, carefully review your policy documents to confirm coverage for hotel expenses under the specific circumstances of your situation. Note any required documentation, deadlines, and claim procedures.

- Gather Necessary Documentation: Collect all relevant documents, including your insurance policy, hotel invoice(s) with itemized expenses, proof of payment, and any supporting documentation related to the unexpected event that necessitated the additional hotel stay (e.g., flight cancellation confirmation, medical certificate).

- Complete the Claim Form: Accurately and completely fill out the claim form provided by your insurance provider. Ensure all information is correct and legible. Inaccurate or incomplete forms are a frequent cause of claim delays or rejection.

- Submit Your Claim: Submit your claim using the preferred method Artikeld by your insurer (online portal, mail, or fax). Keep a copy of all submitted documents for your records.

- Follow Up: After submitting your claim, allow the insurer the processing time specified in your policy. If you haven’t received an update within the stated timeframe, contact your insurer to inquire about the status of your claim.

Common Claim Rejection Reasons and Avoidance Strategies

Claims are sometimes rejected due to various reasons. Understanding these reasons can help prevent rejection.

- Insufficient Documentation: Failing to provide all necessary documentation, such as receipts, confirmations, and policy details, is a primary reason for rejection. Always ensure you have gathered comprehensive documentation before submitting your claim.

- Failure to Meet Policy Requirements: Not meeting the specific conditions and limitations Artikeld in your policy, such as exceeding the maximum coverage amount or failing to report the incident within the stipulated timeframe, can lead to claim denial. Always review your policy carefully.

- Pre-existing Conditions: If the need for additional hotel accommodation stemmed from a pre-existing medical condition not disclosed during policy purchase, the claim might be rejected. Accurate and complete disclosure during policy application is crucial.

- Fraudulent Claims: Submitting false or misleading information will result in immediate claim rejection and may have further legal consequences. Honesty and accuracy are paramount.

Claim Submission Methods

Travel insurance providers offer various methods for submitting claims.

- Online Portal: Many insurers offer secure online portals for convenient claim submission. This method often allows for real-time tracking of claim status.

- Mail: Traditional mail remains an option for submitting claims. Ensure you send your documents via registered mail to maintain proof of submission.

- Fax: Some insurers may accept claims via fax. However, this method is less common now.

Types of Covered Hotel Expenses

Understanding which hotel expenses your travel insurance covers is crucial for a smooth claims process. Policies vary, so carefully reviewing your policy wording is essential. Generally, travel insurance aims to protect you against unforeseen circumstances that disrupt your trip, and this often includes certain hotel-related costs.

Many travel insurance policies cover a range of hotel expenses, but the specifics and limits depend on the policy’s terms and conditions. It’s important to remember that pre-existing conditions or situations known before your trip are typically not covered. This section will Artikel common covered expenses and their typical coverage limits, highlighting situations where additional, less common expenses might be considered.

Covered Hotel Room Charges

Most travel insurance policies cover reasonable and necessary hotel room charges incurred due to covered events, such as trip cancellations or interruptions caused by unforeseen circumstances like severe weather, medical emergencies, or natural disasters. The coverage limit for room charges usually varies depending on the policy and the length of the covered trip interruption. For example, a policy might cover up to $500 per day for a maximum of 5 days, resulting in a total coverage of $2500 for hotel accommodations. This limit often applies to the cost of the room itself, including applicable taxes.

Coverage for Hotel Taxes and Fees

In addition to the base room rate, many policies also cover taxes and mandatory resort fees associated with your hotel stay. These additional costs are typically included within the overall coverage limit for hotel expenses. For instance, if your policy has a $500 daily limit and your room costs $400 plus $50 in taxes and fees, the entire $450 will likely be covered, assuming the incident falls under the policy’s covered events. However, optional fees, such as those for spa services or extra amenities, are generally not included.

Situations Where Additional Expenses Might Be Covered

While hotel room charges and taxes are standard, some policies may extend coverage to additional expenses under specific circumstances. For example, if a covered event necessitates an extended hotel stay, and this extension results in additional meal expenses because you are unable to prepare your own food, these costs might be considered for reimbursement, depending on the policy and the supporting documentation. This is typically subject to a daily limit and overall policy maximum. Another example could be the need for a different hotel due to unforeseen circumstances at the initially booked hotel (e.g., a fire). In such cases, the difference in cost between the original and the replacement hotel might be covered, up to the policy’s limits. Always retain receipts and documentation to support any claim for additional expenses.

Dealing with Delays or Complications

Claim processing times can vary depending on the insurance provider and the complexity of your claim. Unexpected delays can be frustrating, but understanding the potential causes and proactive steps you can take can help mitigate stress and ensure a smoother process. This section Artikels strategies for navigating these challenges.

Dealing with delays often involves patience and persistent communication. It’s important to remember that insurance companies handle a high volume of claims, and unforeseen circumstances can cause temporary backlogs. However, excessive delays warrant proactive intervention.

Delayed Claim Processing

If your claim is taking longer than expected, start by reviewing your policy documents to understand the typical processing timeframe. Contact your insurance provider directly via phone or email, referencing your claim number. Politely inquire about the status of your claim and the anticipated processing date. Keep detailed records of all communication, including dates, times, and the names of individuals you spoke with. If the delay persists beyond a reasonable timeframe (as defined in your policy or through communication with the provider), consider sending a formal written follow-up letter reiterating your concern and requesting an update. In some cases, escalating the issue to a supervisor or a dedicated claims department may be necessary.

Appealing a Rejected Claim

A claim rejection can stem from various reasons, including insufficient documentation, non-compliance with policy terms, or a determination that the expenses aren’t covered. The first step is to carefully review the rejection letter to understand the specific reasons for denial. Gather any additional documentation that might address the concerns raised in the rejection letter. This could include updated medical reports, additional receipts, or clarifying statements. Craft a formal appeal letter, clearly outlining the reasons why you believe the claim should be reconsidered, and include the supporting evidence. Send this appeal via certified mail to ensure proof of delivery. Maintain copies of all correspondence for your records. If the appeal is unsuccessful, consider seeking legal advice if you believe the rejection was unwarranted based on your policy terms.

Communication Challenges with Insurance Providers

Communication difficulties are common when dealing with insurance claims. These can range from difficulties reaching a representative to misunderstandings about policy coverage. To overcome these challenges, maintain detailed records of all communications, including emails, letters, and phone call notes. When contacting the provider, be clear, concise, and organized in your communication. Clearly state your claim number and the specific issue you’re addressing. If you encounter difficulties understanding the information provided, ask for clarification until you are fully satisfied. Consider using email for complex issues, as it provides a written record of the communication. If communication remains problematic, consider seeking assistance from an independent consumer advocacy group or a legal professional. For example, if the provider repeatedly provides inaccurate information about your policy coverage, documenting this inconsistency in writing and escalating it to a supervisor or regulator might be necessary.

Choosing the Right Travel Insurance

Selecting the appropriate travel insurance policy is crucial for ensuring adequate coverage of hotel expenses in unforeseen circumstances. Different providers offer varying levels of protection and associated costs, making a careful comparison essential before purchasing a policy. Understanding the nuances of coverage and policy features will help travelers make informed decisions that best suit their needs and travel plans.

Comparison of Travel Insurance Policies Regarding Hotel Expense Coverage

Travel insurance policies vary significantly in their coverage of hotel expenses. Some policies offer comprehensive coverage for cancellations, interruptions, and emergencies, while others provide more limited protection. Factors such as the policy’s terms and conditions, the type of trip, and the traveler’s pre-existing medical conditions all influence the extent of coverage. It’s vital to carefully review the policy wording to understand what is and is not covered. For example, some policies may only cover hotel expenses resulting from specific covered events, such as flight cancellations due to inclement weather, while others may extend coverage to a broader range of circumstances.

Key Features of Comprehensive Hotel Expense Coverage

Several key features should be considered when selecting a travel insurance policy with comprehensive hotel expense coverage. These features help to ensure that the policy adequately protects travelers against potential financial losses related to hotel accommodations. Prioritizing policies with clear and unambiguous language regarding hotel expense coverage is crucial.

| Policy Provider | Coverage Details | Premium Costs (Example) |

|---|---|---|

| Example Provider A | Covers hotel expenses due to trip cancellation, interruption, or medical emergency. Maximum coverage of $5,000. Requires pre-existing condition disclosure. | $100 |

| Example Provider B | Covers hotel expenses due to flight delays exceeding 12 hours. Maximum coverage of $2,000. No pre-existing condition disclosure required. | $75 |

| Example Provider C | Covers hotel expenses due to natural disasters impacting the hotel. Maximum coverage of $3,000. Includes coverage for alternative accommodation. | $125 |

Note: Premium costs are illustrative examples and will vary based on factors such as trip duration, destination, and traveler age. Always check the specific policy details for accurate pricing and coverage information. The examples above are hypothetical and do not reflect any specific insurance provider’s offerings.

Prevention Strategies

Proactive measures significantly reduce the likelihood of needing to file a travel insurance claim for hotel expenses. By carefully planning your trip and selecting accommodations wisely, you can minimize the chances of encountering unexpected issues and associated costs. This section Artikels practical strategies to help you avoid problems before they arise.

Preventing hotel expense issues begins long before your trip. Careful planning and verification can save you significant stress and potential financial losses. Understanding your needs and expectations is key to choosing the right hotel and avoiding unforeseen problems.

Selecting Reputable Hotels

Choosing a reputable hotel is the first line of defense against many potential problems. Reputable hotels generally have established processes for handling guest concerns and are more likely to provide the services and amenities they advertise. This minimizes the risk of disputes and unexpected expenses. Consider using well-known hotel chains or independently researching hotels through reliable review websites. Pay close attention to guest reviews, focusing on comments about cleanliness, service, and accuracy of advertised amenities. Checking ratings from multiple sources provides a more comprehensive picture of the hotel’s reputation. For example, a hotel with consistently high ratings across several review platforms is more likely to be a reliable choice than one with mixed or predominantly negative reviews.

Verifying Hotel Bookings and Confirming Amenities

Once you’ve selected a hotel, it’s crucial to verify your booking and confirm that it includes all the amenities you expect. This includes carefully reviewing your booking confirmation to ensure the dates, room type, and number of guests are accurate. Contact the hotel directly to confirm your reservation and inquire about any specific amenities, such as Wi-Fi access, parking, or breakfast inclusions. This direct communication helps clarify any ambiguities and prevents misunderstandings that could lead to unexpected charges upon arrival. For example, if you require a crib for your baby, confirm availability and any associated fees in advance. Similarly, if you are travelling with a pet, ensure that the hotel permits pets and understand any applicable charges.

Preventative Measures to Avoid Unexpected Hotel Expenses

Several preventative measures can further minimize the risk of unexpected hotel expenses. These include understanding the hotel’s cancellation policy and purchasing travel insurance with comprehensive coverage. Reading the fine print of your booking carefully, including understanding any extra charges for services like early check-in or late check-out, is also crucial. Additionally, be aware of potential hidden fees or additional charges, such as resort fees or parking fees. Keeping a record of all your transactions, including receipts for any incidental expenses incurred at the hotel, will also prove beneficial should any issues arise. Finally, reporting any problems or concerns to the hotel management immediately allows them to address the issue and prevents minor problems from escalating into significant expenses.

Understanding Exclusions and Limitations

Travel insurance policies, while designed to offer comprehensive coverage, often include exclusions and limitations that restrict the scope of their protection. Understanding these limitations is crucial to avoid disappointment and ensure you’re adequately protected when claiming hotel expenses. Failing to understand these clauses can lead to a denied claim, even if you believe you are entitled to compensation.

It’s important to remember that travel insurance is not a guarantee of reimbursement for all expenses incurred during a trip. Instead, it acts as a safety net for unforeseen circumstances, and the specific details of what’s covered are determined by the policy’s terms and conditions.

Common Exclusions Related to Hotel Expenses

Many travel insurance policies exclude certain types of hotel expenses from coverage. These exclusions are often clearly stated within the policy document. Familiarizing yourself with these limitations is key to making informed decisions and avoiding costly surprises.

- Pre-existing medical conditions: If your hotel stay is extended due to a pre-existing medical condition, the additional expenses may not be covered. Policies typically require that the need for extended accommodation is a direct result of a covered event, such as a sudden illness unrelated to a pre-existing condition.

- Acts of negligence: Expenses incurred due to your own negligence or recklessness, such as losing your hotel key and incurring replacement fees, are usually not covered.

- Force majeure events (with specific limitations): While some policies cover expenses resulting from force majeure events (like natural disasters), there might be limitations. For instance, coverage may be capped at a certain number of days or exclude certain types of events.

- Non-emergency situations: If you simply choose to extend your hotel stay for personal reasons, these extra expenses are typically not covered. The need for extended accommodation must usually stem from a covered event as Artikeld in your policy.

- Fraudulent claims: Any attempt to defraud the insurance provider by falsely claiming hotel expenses will result in a claim denial and potentially further legal consequences.

Implications of Exceeding Coverage Limits

Each travel insurance policy has specific coverage limits for hotel expenses. These limits represent the maximum amount the insurer will pay for covered hotel expenses related to a specific event. Understanding these limits is vital in planning your trip and budgeting accordingly.

Exceeding these limits means you will be responsible for the difference between the actual expenses and the policy’s coverage limit. For example, if your policy covers up to $500 for additional hotel expenses due to flight delays, and your actual expenses reach $700, you will have to pay the remaining $200 yourself.

Understanding Policy Wording and Identifying Ambiguities

Travel insurance policies often use specific legal terminology. It’s crucial to carefully read and understand the policy wording, paying close attention to definitions, exclusions, and limitations. If you encounter ambiguous language or unclear clauses, don’t hesitate to contact your insurance provider for clarification. It’s always better to seek clarification before an incident occurs.

For instance, a policy might state coverage for “reasonable and necessary” hotel expenses. Understanding what constitutes “reasonable and necessary” in the context of your specific situation is vital. If in doubt, keep detailed records and receipts and contact your insurer to discuss your potential claim before incurring significant additional expenses.

Using Technology to Streamline the Process

In today’s digital age, technology offers significant advantages in managing travel insurance claims, particularly those related to hotel expenses. Utilizing various digital tools can expedite the process, improve communication with your provider, and ultimately reduce stress during an already challenging situation. From mobile apps to online portals, these technologies simplify the complexities of filing a claim and tracking its progress.

The integration of technology into the travel insurance claims process offers numerous benefits, including faster claim processing times, increased transparency, and enhanced accessibility. By leveraging these digital tools, you can significantly improve the efficiency and convenience of your claim submission and management.

Mobile Apps for Claim Submission and Progress Tracking

Many travel insurance providers now offer dedicated mobile applications designed to streamline the claims process. These apps typically allow policyholders to submit claims directly from their smartphones, upload supporting documentation (such as photos of damaged luggage or hotel receipts), and track the status of their claim in real-time. This eliminates the need for cumbersome paperwork and lengthy phone calls, offering a more efficient and user-friendly experience. For example, a hypothetical app, “TravelSafe,” might allow users to submit a claim with just a few taps, including uploading photos of their hotel confirmation and a copy of their damaged passport. The app would then provide regular updates on the claim’s progress via push notifications.

Online Portals for Managing Travel Insurance Policies

Online portals provide a centralized location for managing all aspects of your travel insurance policy. Through these portals, you can access your policy details, view coverage information, submit claims, and track their progress. This eliminates the need to contact your provider via phone or email for simple inquiries, allowing for self-service management of your policy. For instance, a policyholder could log into their provider’s online portal to instantly download a copy of their policy documents or check the status of a pending claim without having to wait for a response from a customer service representative.

Digital Receipts for Simplified Claim Submission

The use of digital receipts can significantly simplify the claim submission process. Instead of relying on physical receipts that can be easily lost or damaged, digital receipts stored on your smartphone or in cloud-based services provide readily available proof of purchase. This eliminates the need to search for physical receipts and ensures that all necessary documentation is readily available when submitting your claim. Consider a scenario where a traveler uses a mobile payment app to pay for their hotel stay. The digital receipt automatically saved to their phone can be easily uploaded to their travel insurance claim, providing immediate proof of purchase and cost.

Contacting Your Insurance Provider: How To Claim Hotel Expenses Through Your Travel Insurance Provider

Effective communication is crucial when filing a claim for hotel expenses with your travel insurance provider. A clear and organized approach ensures a smoother process and increases the likelihood of a successful claim. This section will Artikel effective communication strategies and the importance of maintaining detailed records.

Effective communication involves clearly articulating your situation, providing all necessary documentation, and maintaining a professional and polite demeanor throughout the process. Remember, the insurance provider is there to assist you, and a collaborative approach will yield better results.

Effective Communication Strategies

Employing clear and concise language when contacting your insurance provider is paramount. Avoid jargon and explain your situation in a straightforward manner. For instance, instead of saying “My hotel stay was impacted by unforeseen circumstances,” you could state, “Due to a flight cancellation caused by a severe storm, I was forced to extend my hotel stay by two nights.” Providing specific dates, times, and relevant details will significantly aid the claims process. Additionally, using a formal tone and maintaining a respectful attitude will contribute to a positive interaction. If you have questions, list them in a clear, numbered format to ensure all concerns are addressed.

Maintaining Detailed Records of Communication

Meticulously documenting all communication with your insurance provider is essential. This includes retaining copies of emails, letters, and notes from phone conversations. This documentation serves as a valuable record in case of disputes or delays. For each interaction, note the date, time, the individual you spoke with (if applicable), a summary of the conversation, and any agreements or next steps. This detailed record provides a chronological history of your claim and allows you to refer back to specific information quickly.

Escalation Process for Unsuccessful Initial Communication

If your initial communication with your insurance provider does not yield a satisfactory resolution, you have options for escalation. If you are unsatisfied with the response from your initial point of contact, you can request to speak to a supervisor or manager. Many insurance providers have clearly defined escalation procedures Artikeld on their website or within their policy documents. If the issue remains unresolved, you may consider contacting your state’s insurance commissioner or filing a complaint with the Better Business Bureau. These third-party organizations can often help mediate disputes and ensure fair treatment. Keep in mind that each insurance provider will have its own internal escalation process; therefore, reviewing your policy or contacting customer service for guidance is highly recommended.

Illustrative Examples of Successful Claims

Understanding how travel insurance works in practice can be greatly aided by reviewing successful claims. The following examples illustrate how different types of hotel expense issues were successfully resolved through travel insurance. Remember that specific coverage details vary by policy, so always refer to your policy documents for complete information.

Successful Claim: Flight Cancellation Leading to Extended Hotel Stay

Ms. Emily Carter booked a non-refundable hotel stay at the Grand Hyatt, San Francisco, for a three-night business trip. Due to unforeseen severe weather conditions, her flight was canceled, resulting in a two-night extension of her hotel stay. Ms. Carter promptly contacted her travel insurance provider, WorldTravelSafe, providing documentation including her flight cancellation confirmation from the airline, her original hotel booking confirmation, and the updated hotel invoice reflecting the extra two nights. WorldTravelSafe reviewed the documentation and approved her claim, reimbursing her for the additional hotel costs. The Grand Hyatt was a luxury hotel known for its excellent location and amenities near the San Francisco financial district. The claim was processed smoothly due to the clear and complete documentation provided.

Successful Claim: Hotel Room Damage Due to Unforeseen Circumstances, How to Claim Hotel Expenses Through Your Travel Insurance Provider

Mr. David Lee, while staying at the Comfort Inn, Orlando, experienced a burst pipe in his room due to a sudden plumbing failure. The resulting water damage rendered the room uninhabitable. Mr. Lee immediately reported the incident to the hotel management and obtained a written report documenting the damage and the hotel’s subsequent relocation of him to another room. He also kept all receipts for any additional expenses incurred due to the incident. He submitted these documents, along with photos of the damage, to his insurer, TravelSecure. TravelSecure investigated the claim and, upon verification, reimbursed Mr. Lee for the expenses related to the incident, including the cost difference between the original room and the replacement room. The Comfort Inn is a mid-range hotel chain known for its consistent service and comfortable accommodations. The successful claim was facilitated by Mr. Lee’s prompt reporting and detailed documentation.

Successful Claim: Medical Emergency Requiring Extended Hotel Stay

During a family vacation in London, Mrs. Sarah Miller’s child fell ill and required hospitalization. The family’s pre-booked stay at the Premier Inn, London Heathrow, was extended due to the child’s medical emergency and the need for prolonged care. Mrs. Miller submitted a comprehensive claim to her insurer, GlobalTravelAssist, including medical bills, the child’s hospital discharge summary, and the updated hotel invoice. GlobalTravelAssist, after reviewing the medical documentation and the hotel invoices, approved the claim, covering the additional hotel costs incurred during the medical emergency. The Premier Inn is a budget-friendly hotel chain with locations conveniently near major transportation hubs. The successful claim highlighted the importance of comprehensive travel insurance, particularly for families.

Question & Answer Hub

What if my hotel burns down and I need a new hotel?

Most travel insurance policies cover unforeseen circumstances like hotel fires, provided you can prove the event and your resulting need for alternative accommodation. Keep all documentation, including police reports if applicable.

Can I claim for meals if my hotel is uninhabitable due to unforeseen circumstances?

Depending on your policy, some may cover necessary meal expenses if your hotel becomes uninhabitable due to an unforeseen and covered event. Check your policy details for specific coverage.

What happens if my claim is denied?

Review the denial reason carefully. If you disagree, contact your insurer to appeal the decision. Provide additional documentation or clarify any misunderstandings. Keep records of all communication.

How long does the claim process typically take?

Processing times vary depending on the insurer and the complexity of the claim. Check your policy for estimated processing times and contact your insurer for updates if necessary.